Posted on

May 15, 2023

by

Eugene Palermo

As forecast March’s residential resale market continued its upward trajectory, constrained only by available supply and the lack of affordability driven by the high cost of mortgage financing and the requirement to stress-test borrowers. Stress testing means that buyers must qualify at 2 percent higher than the interest rate of the mortgage they are seeking. In March the five-year fixed-term mortgage interest rate was slightly below 5 percent. Buyers, therefore, must qualify at approximately 7 percent.

Notwithstanding these constraints, 6,896 properties were reported sold. March saw the second consecutive monthly increase in sales from the lows of December and January.

February’s 4,765 reported sales represented a 54 percent increase compared to January’s 3,089 sales, while March’s 6,896 sales saw a 45 percent jump in sales compared to February. If the market continues at its current pace April’s sales may come in at close to 8,000 which will exceed the 7,226 reported sales in May 2022, the last month that saw more than 7,000 sales.

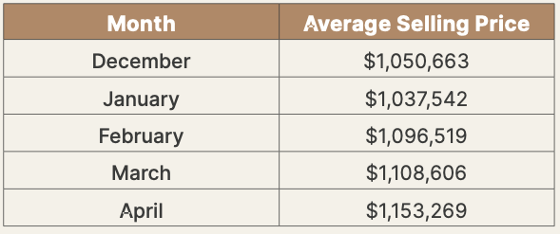

Like reported sales, average sale prices also continue to rise.

February’s average sale price was almost 6 percent higher than the average sale price for all properties sold in January, while March’s average sale price at $1,108,606 was 1 percent higher than the price achieved in February. March’s average sale price was the highest achieved since June of 2022. Until the Bank of Canada begins to reduce its benchmark rate, currently at 4.5 percent, average sale prices will increase very moderately. Buyers’ ability to pay higher prices will be constrained by the prevailing punishing mortgage interest rates and the stress testing imposed by the Office of Superintendent of Financial Institutions.

The Bank of Canada is not expected to reduce its benchmark rate until late 2023. If inflation persists the benchmark rate will only start to be lowered in 2024. Collectively most economists affiliated with Canada’s big banks are of the view that even by the end of 2024 the benchmark rate will at best be at 3 percent. By then the “cheap” money available during the pandemic will be a distant memory.

High financing costs and supply are the key factors influencing the residential resale market. In March only 11,184 new properties came to market, far too few to meet demand. Last year 20,061 came to market in March, a year-over-year decline of almost 45 percent. On the back of immigration population growth in Toronto and the surrounding region continues at a record pace increasing the growth of demand against a dwindling level of supply.

This tension, between supply and demand, is nowhere more evident than in March’s resale data. Throughout the greater Toronto region all properties sold (on average) in only 19 days. Not only did they sell quickly, but they sold for 101 percent of their asking price. The first time this has happened since May of 2022. Reported sales in Toronto’s eastern trading areas were even faster: all properties sold in only 15 days and at 107 percent of their asking price. Semi-detached properties in the same trading areas sold in a shocking 12 days and at 113 percent of their asking price. These statistics are comparable to market movement during the height of the pandemic. Those economists that predicted a market bubble and crash are going to be sorely disappointed.

These numbers also speak to increasing levels of competition amongst buyers. Multiple offers are once again becoming the norm, particularly in desirable neighbourhoods. There are simply too many buyers for too few available properties. For example: in the City of Toronto there were only 215 available semi-detached properties for sale at the end of March. In March 202 semi- detached properties were reported sold. Effectively all semi-detached properties that came to market in March sold in the same month. Most semi-detached properties that sold did so in competition. All detached properties sold in only 16 days at 102 percent of their asking price, at an average sale price of $1,708,373.

The only real supply in the City of Toronto is in the condominium sector. At the end of March there were 4,292 properties in total available for sale in the City of Toronto (and 10,120 throughout the greater Toronto area). More than 62 percent of all listings in the City of Toronto (2,675) are condominium apartments. In March 1,410 condominium apartments were sold in the City of Toronto, with another 711 condominium apartment sales in the 905 region. Although condominium apartment sales were not as robust as ground-level property sales, they did sell for 100 percent of their asking price and in 22 days, 3 days longer than the overall average of 19 days on market. The average sale price of all condominium apartments came in at $732,944, and $786,694 for sales in Toronto’s central core, where most condominium apartments are located.

Looking toward April we anticipate further increases in the number of properties reported sold, perhaps as high as 8,000, and average sale prices rising, but moderately, constrained by the high cost of mortgage financing. Barring any unforeseen economic changes this should be the resale market’s pattern for the remainder of 2023. The Toronto and region resale marketplace can be summed up as follows – high levels of demand constrained by low levels of supply and affordability.

Posted on

May 15, 2023

by

Eugene Palermo

As forecast in March’s Market Report, April’s residential resale market continued its upward trajectory for the third month in a row. Sales volumes increased by more than 9 percent compared to March and the average sale price, which also bounced for the third month in a row since January, increased by more than 3 percent compared to March.

This trajectory is unlikely to change in May. It would have been even steeper if not constrained by affordability and the alarming decline in supply.

Although April’s 7,531 residential sales were 5.2 percent less than the 7,940 sales achieved last year, they reflect growing buyer confidence and acceptance that the exceptionally low financing costs enjoyed during the pandemic are a thing of the past. Demand has not abated, pushed to extraordinarily high levels by growth in population in the greater Toronto region, driven years of high levels of immigration. Between the years 2018 and 2022, more than 600,000 immigrants have moved into southern Ontario. New housing supply has not kept pace with this growth in population.

As a result of the eye-popping demand, average sale prices continue to rise in April, even in the face of high mortgage financing costs and borrower stress testing which adds 2 percent to the interest rate at which borrowers are attempting to qualify. April’s average sale price of $1,153,269 was only 7.8 percent lower than the average sale price achieved in April 2022. When interest rates begin to decline, which is expected in 2024, we could see average sale prices increasing to the stratospheric heights achieved during the pandemic. Six months ago this possibility was inconceivable.

The number of new properties coming to market became even more troubling during April. In April only 11,364 new listings became available to the many buyers waiting to buy. This is a 38 percent decline compared to the 18,416 properties that came to market last April. More troubling is the available supply as April came to an end. At the end of April, there were only 10,373 active listings, more than 20 percent less than the 13,092 properties available to buyers at the end of April last year. April marked the first month since March of last year when active listings were fewer than the corresponding month the year before.

Given the demand and the lack of supply in the greater Toronto area, it is not surprising that all available properties (on average) sold in only 17 days. The speed at which properties sold in April is quickly approaching the speed with which properties in the greater Toronto area sold during the height of the pandemic market – 8 days! All properties in the City of Toronto sold in only 18 days (slightly slower due to the preponderance of condominium apartment sales) but incredibly for 103 percent of their asking prices. In Toronto’s eastern districts all properties, condominium apartments, detached and semi-detached properties sold in only 11 days and for an eye-popping 109 percent of their asking prices. Semi-detached properties in the eastern districts sold in only 8 days at 115 percent of their asking prices. The average sale price of semi-detached properties in Toronto’s eastern districts was $1,223,687. Across all of Toronto the average sale price for semi-detached was $1,326,462. Detached properties came in at $1,787,752.

Shockingly there were seven eastern districts that reported less than five semi-detached property sales – simply because there was no supply!

Fast sales and sale prices exceeding asking prices were not restricted to the City of Toronto. All property sales in Halton, York, and Durham region sold well above their asking prices, 101, 105, and 107 percent above asking, respectively, with all properties selling (on average) after only 15 days on the market.

The Toronto and region residential resale market is quickly moving towards crisis levels. Governments now have no one to blame but themselves, and hopefully are beginning to accept that the housing crisis can not be improved by restrictive legislation. At the federal level, there is a prohibition on foreign buyers purchasing residential properties in Canada. At the provincial level, there is a 25 percent (of the purchase price) tax on foreign buyers. At the municipal level (City of Toronto) there is a 1 percent vacancy tax. None of these legislative actions have addressed Toronto and the region’s housing issues. Toronto’s resale market is driven by domestic demand, as numerous studies have demonstrated. Population growth, which is expected to continue, requires appropriate levels of new housing, which have not been forthcoming. It is safe to forecast that the residential resale conditions that have clearly manifested themselves in April will continue and intensify as we move towards the second half of 2023.

Categories:

Annex, Toronto C02 Real Estate

|

Bay Street Corridor, Toronto C01 Real Estate

|

Bedford Park-Nortown, Toronto C04 Real Estate

|

Blake-Jones, Toronto E01 Real Estate

|

Cabbagetown-South St. James Town, Toronto C08 Real Estate

|

Church-Yonge Corridor, Toronto C08 Real Estate

|

Crescent Town, Toronto E03 Real Estate

|

Edenbridge-Humber Valley, Toronto W08 Real Estate

|

Eringate-Centennial-West Deane, Toronto W08 Real Estate

|

High Park-Swansea, Toronto W01 Real Estate

|

July 2025 Toronto Real Estate Market Report

|

Mimico, Toronto W06 Real Estate

|

Moss Park, Toronto C08 Real Estate

|

Niagara, Toronto C01 Real Estate

|

North Riverdale, Toronto E01 Real Estate

|

North St. James Town, Toronto C08 Real Estate

|

Playter Estates-Danforth, Toronto E03 Real Estate

|

Regent Park, Toronto C08 Real Estate

|

South Riverdale, Toronto E01 Real Estate

|

The Beaches, Toronto E02 Real Estate

|

Toronto C01 Real Estate

|

Toronto C08 Real Estate

|

Toronto E06 Real Estate

|

Waterfront Communities C1, Toronto C01 Real Estate

|

Waterfront Communities C8, Toronto C08 Real Estate

|

Yonge-St. Clair, Toronto C02 Real Estate

This website may only be used by consumers that have a bona fide interest in the purchase, sale, or lease of real estate of the type being offered via the website.

The data relating to real estate on this website comes in part from the MLS® Reciprocity program of the PropTx MLS®. The data is deemed reliable but is not guaranteed to be accurate.